Banks vs. Stablecoins: The Fight Over Yield

On April 8, 2026, the White House Council of Economic Advisers published a 21-page paper with a single finding at its core.

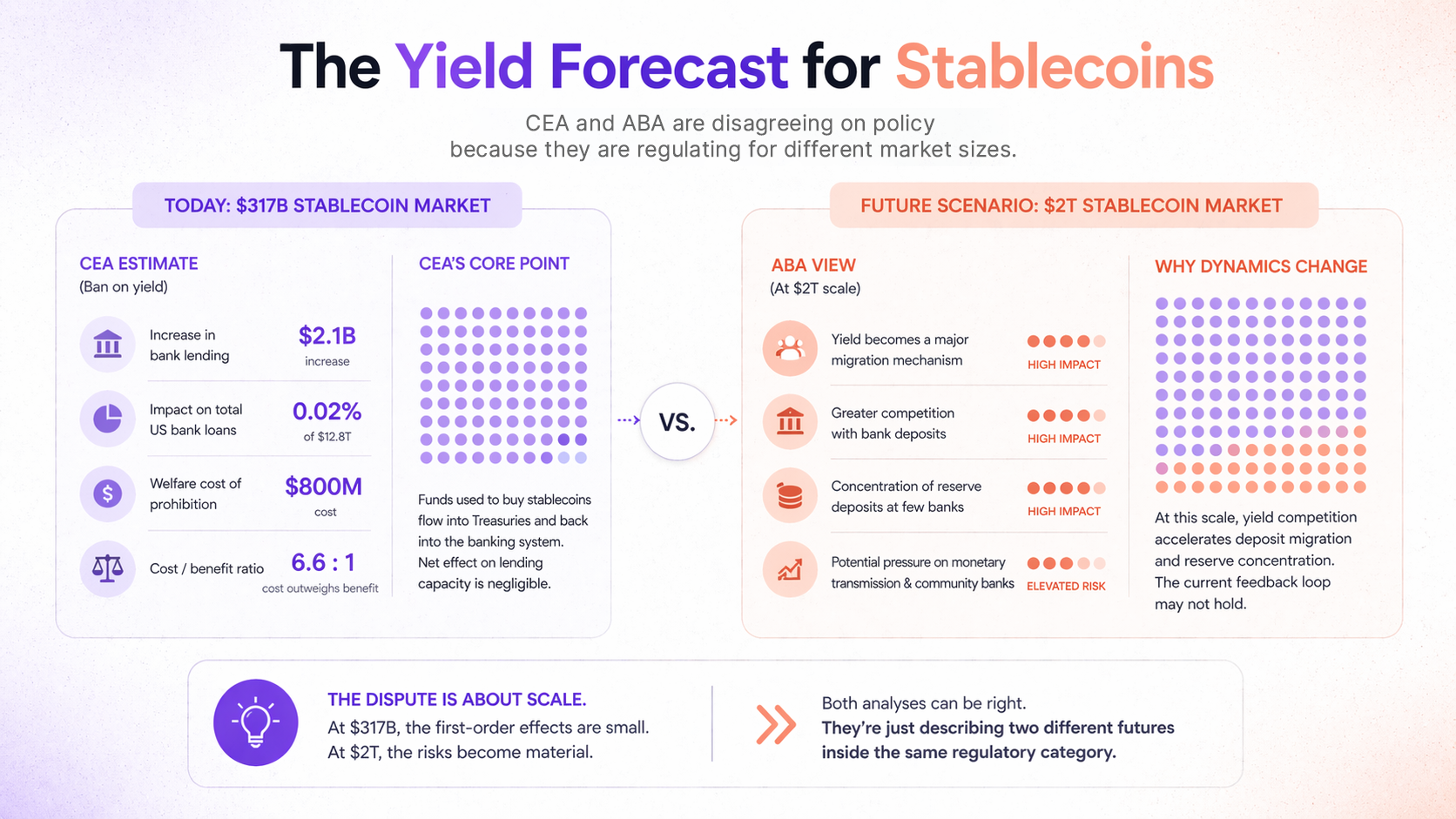

Banning yield on stablecoins, the paper concluded, would increase bank lending in the United States by $2.1 billion. In a financial system with roughly $12.8 trillion in outstanding bank loans, that is an increase of 0.02%. The welfare cost of the prohibition, by the CEA's own calibration, is $800 million. The ratio of cost to benefit, the paper notes plainly, is 6.6 to 1.

The American Bankers Association replied five days later. Its counterargument was not that the CEA's arithmetic was wrong. It was that the CEA had modelled the wrong scenario. Measure the effect of a yield ban on today's $317 billion stablecoin market and the numbers are indeed small. Measure the effect on a $2 trillion stablecoin market, the trajectory Standard Chartered and others have projected by 2028, and the picture changes. "In a larger market," the ABA wrote, "yield is not a minor product feature; it is the mechanism that would accelerate migration out of bank deposits."

Two days after that, senators announced a deal in principle with the White House to resolve the question inside the Digital Asset Market Clarity Act. What the compromise looks like remains to be seen. What the debate has already revealed is that Washington has spent eighteen months trying to answer a design question with a prohibition, and the answer it reaches will shape how dollar stablecoins compete with bank deposits for the next decade.

Europe resolved this question two years ago, in the opposite direction and with far less debate. MiCA Articles 45(1) and 50 prohibit any interest, discount, or benefit tied to the duration of holding a stablecoin, whether granted by the issuer or by the crypto-asset service providers distributing it. The European regulator did not need a 21-page welfare calculation. The prohibition was inherited from the E-Money Directive, which has forbidden interest-bearing e-money since 2009 precisely to prevent e-money from functioning as a substitute for bank deposits. Under MiCA, at least 30% of an EMT issuer's reserves must sit in deposits at credit institutions. The remaining reserves can be held in highly liquid instruments denominated in the same currency as the token.

The two jurisdictions have now reached opposite conclusions on the same underlying question. That divergence deserves closer analysis than it has received.

What is actually being regulated

The yield debate is framed as a consumer-welfare question. It is better understood as a question about what a stablecoin is.

A stablecoin with no yield is a payment instrument. It moves value between counterparties, settles obligations, and denominates transactions. Its utility derives from liquidity, acceptance, and settlement speed. Holders do not expect return. They expect redemption at par.

A stablecoin that pays yield is something else. The mechanics look identical. The user holds a tokenized liability of an issuer, backed by reserve assets. What changes is the economic relationship. A yield-bearing stablecoin is a claim on the return generated by the reserve portfolio. It functions, in substance, as a money market fund distributed on blockchain infrastructure. The reserve composition matters not just for solvency but for yield. The holder is no longer a user of a payment instrument. The holder is a depositor in a narrow bank, or a shareholder in a tokenized fund.

Regulators on both sides of the Atlantic have spent eighteen months deciding whether they are regulating the first thing or the second. The GENIUS Act and MiCA both prohibit yield from the issuer. Both preserve, with different degrees of clarity, the ability of third parties to pay return on stablecoin holdings through affiliated programs. The CLARITY Act negotiations have been hung up on exactly how wide that third-party channel should remain. The ABA's real concern, stripped of rhetoric, is that leaving the channel open creates a pathway for stablecoins to compete with deposits at scale. The crypto industry's real concern is that closing the channel reduces stablecoins to a payments product with no economic incentive for holders.

Both concerns are accurate. They describe two different products, both plausibly called a stablecoin.

The economic logic of prohibition

The case for prohibiting yield rests on a specific chain of reasoning. If stablecoins pay yield competitive with bank deposits, depositors shift funds from banks to stablecoins. Because stablecoin reserves must be fully backed rather than fractionally lent, that shift reduces the pool of deposits available for bank lending. Less lending means less credit creation, tighter conditions for households and small businesses, and weakened transmission of monetary policy.

The CEA's paper challenges this chain at its weakest link. The logic assumes that funds used to buy stablecoins leave the banking system permanently. In practice, those funds are redeposited. An issuer receiving $1 billion in purchases places the proceeds into Treasury bills or, under MiCA, into bank deposits. The Treasury bill issuer or the receiving bank then holds those funds. The aggregate deposit base does not shrink. Its composition shifts. Lending to households reroutes through a different intermediary chain, but the chain still exists.

This is the CEA's core point, and it is correct within the assumptions of its model. Under the baseline, prohibiting yield produces a 0.02% increase in lending because the first-order effect the banks warn about does not actually materialize. Funds flow through stablecoin reserves into Treasuries and back into the banking system. The net effect on lending capacity is negligible.

The ABA's rebuttal is that the model is calibrated to a market roughly one-sixth the size the banking industry expects stablecoins to reach. At $2 trillion, the dynamics shift. Large issuers would concentrate reserve deposits at a small number of banks, disadvantaging community lenders. Yield competition would accelerate migration from lower-rate deposit accounts. The Fed's monetary framework, which currently recycles stablecoin reserves back into the banking system through money market operations, might not hold under that scale.

The dispute is not resolvable through calibration. It is a dispute about which version of the future to regulate for.

Why Europe chose prohibition without debate

MiCA did not arrive at its prohibition through a welfare calculation. It arrived at it through the logic of the E-Money Directive, which has structured European payment regulation for fifteen years. The principle underlying the EMD was simple. Electronic money is a claim on the issuer for immediate redemption at par. A claim that pays interest is a deposit. Deposits are regulated under the Capital Requirements Regulation, not under the EMD. Allowing e-money to pay interest would collapse the boundary between e-money institutions and credit institutions, and would require either extending bank-grade supervision to EMIs or weakening the protections around bank-like activity.

MiCA inherited this logic wholesale. An EMT is defined in Article 3 as a crypto-asset that aims to maintain a stable value by referencing a single official currency. It is electronic money expressed through distributed ledger technology. The prohibition on interest under Article 50 extends the EMD principle to the tokenized form. The 30% minimum reserve in bank deposits under Article 54 ensures that even the reserve management of an EMT issuer is tethered to the banking system rather than competing with it.

The European framework is internally consistent. It treats stablecoins as a payment instrument and regulates them accordingly. It does not attempt to calculate the welfare trade-off between consumer yield and bank lending because that trade-off does not arise within its conceptual architecture. A stablecoin that pays yield is not a permitted product. The category does not exist.

This consistency has a cost. It means that a European user holding a MiCA-compliant EMT receives no return on reserves that may be earning 3% or more in underlying instruments. It means that an issuer cannot differentiate through yield. It means that euro-denominated stablecoins compete with dollar-denominated alternatives on liquidity, acceptance, and settlement speed alone, and dollar stablecoins already hold structural advantages in all three.

Why the US debate is unresolved

The United States does not have a fifteen-year regulatory tradition treating stablecoins as e-money. It has two legislative frameworks trying to answer a question Europe answered by inheritance. The GENIUS Act prohibits direct yield from the issuer but leaves affiliate arrangements ambiguous. The CLARITY Act is meant to close that ambiguity, but has stalled because closing it in either direction produces winners and losers that the political system has not yet metabolized.

The winners of a strict prohibition are banks, whose deposit franchise is protected from a new class of competitor. The losers are consumers, who forgo yield on assets that are already, in effect, earning yield inside issuer reserves. The winners of a permissive regime are crypto-native platforms, which can distribute yield through affiliate programs. The losers are, again, banks, who face deposit migration at scale. The CEA's paper made the case that the losses to banks are overstated. The ABA responded that the losses are being measured against the wrong baseline.

Neither side of this argument is principally about consumer welfare. Both sides are about who gets to be the intermediary between deposits and Treasury yield. Banks have held that position for a century through deposit insurance and fractional reserve lending. Stablecoin issuers have taken a version of it, with full reserve backing and direct Treasury holdings, over roughly five years. Tether and Circle together hold Treasury bill portfolios comparable to the top twenty money market funds in the world. They are, by any functional definition, already in the business banks are trying to protect. The yield question is the question of whether they can scale that business to retail users at competitive return.

The design problem regulators are avoiding

The real question under both frameworks is not whether stablecoins should pay yield. It is whether payment instruments and money market instruments should continue to be regulated as if they were different products when tokenization has made them mechanically indistinguishable.

A tokenized money market fund and a yield-bearing stablecoin look identical to the holder. Both offer dollar-denominated liquidity with interest accrual. Both are redeemable at par plus yield. Both settle on public blockchains. The regulatory categories that separate them, securities law on one side, e-money and payments law on the other, were designed for a financial system in which the products they governed had materially different operating characteristics. In a tokenized system, those characteristics converge.

Neither MiCA nor GENIUS has addressed this convergence. MiCA solved the yield question by adopting a prohibition inherited from pre-tokenization e-money law. GENIUS solved it by prohibiting issuer yield while leaving a channel open for affiliate distribution, creating the ambiguity that CLARITY is now trying to resolve. Both frameworks are treating stablecoins as a product category, when the more productive question is whether the category itself still holds.

The answer a properly designed framework would give is that regulators should distinguish between stablecoins used for payments and stablecoins used as a store of value. The first category needs fast settlement, broad acceptance, and redemption certainty. Yield is not required and arguably not desirable, because holding duration should be incidental to payment utility. The second category needs transparent reserve management, yield pass-through, and investor-protection disclosures. These are money market products distributed on new rails, and they should be regulated as such.

Neither framework has taken this step. MiCA treats all stablecoins as the first category and prohibits the second. GENIUS treats all stablecoins as the first category and leaves the second to regulatory improvisation. The CLARITY fight is what improvisation looks like when the underlying categories have not been redrawn.

Position

The yield debate is framed as a fight between banks and crypto firms. It is better understood as the visible symptom of a framework problem regulators have not yet acknowledged. Stablecoins are not one product. They are a container for several products with different economic functions, which happen to share a token standard. Regulating the container produces the stand-off now playing out in the Senate and the structural constraint now limiting euro stablecoin competitiveness.

The eventual resolution will require separating the categories. Payment stablecoins should be regulated as e-money, with reserve requirements, redemption rights, and no yield. Yield-bearing stablecoins should be regulated as tokenized money market instruments, with investor protections, transparent reserve disclosure, and explicit acknowledgment of their substitutive relationship to deposits and money market funds. Both categories can be MiCA-compliant. Both can be GENIUS-compliant. But they cannot be the same product, regulated under the same article, producing the same welfare analysis.

The CEA paper is the most careful economic analysis of this question published so far. Its conclusion that a yield prohibition produces negligible benefits to bank lending is almost certainly correct at current market scale. The ABA's rebuttal that the dynamics change at $2 trillion is almost certainly correct at scale. Both can be true because they are describing two different products inside a single regulatory category. The design flaw is in the category, not in the analysis.

Europe's prohibition is cleaner. Washington's improvisation is more honest about the problem. Neither has solved it. Whichever jurisdiction separates the categories first will produce the framework the other eventually adopts.

Latest Articles

.avif)

.avif)

.avif)

.webp)

Join 20,000+ businesses already growing

We build and integrate solutions. You grow with xMoney.